Double Standards or Principles? Why the US & EU Trade with Russia While Criticizing India

The US & EU still import goods from Russia like uranium, LNG, & fertilizers while criticizing India’s Russian oil trade. Double Standards or Principles?

When Russia invaded Ukraine in February 2022, the United States and the European Union positioned themselves as champions of democratic values, rallying behind sanctions meant to choke off Moscow’s ability to finance its war. Leaders spoke of unity, resolve, and the moral imperative of cutting economic ties. But three years later, in 2025, the reality of global trade paints a messier picture, one that reveals glaring contradictions, as per the global trade data. While Washington and Brussels condemn other nations, especially India, for doing business with Russia, they continue importing billions of dollars’ worth of Russian goods. And they’re doing so not in obscure categories, but in strategic commodities central to their economies: uranium, fertilizers, palladium, natural gas, and more. Recently, President Donald Trump announced a 50% tariff on Indian goods due to India’s continued trade with Russia, contributing to the India-US trade tensions.

Since February 2022, the West’s public stance on Russia has been crystal clear: condemn the invasion of Ukraine, cut off Moscow’s economic lifelines, and isolate it from the global marketplace. In press conferences, speeches, and policy briefings, both Washington and Brussels have stressed unity, resolve, and the urgency of “starving the Russian war machine.” Yet, behind the rhetoric, trade flows tell a different story. By 2025, while Russia’s overall exports to the US and EU had fallen sharply compared to pre-war levels, billions of dollars in critical goods still move westward, legally, openly, and often under exemptions that rarely make it into headlines.

Meanwhile, India, which purchases discounted Russian oil and sells refined products to the global market, is routinely chastised by US and EU officials for “funding Putin’s war.” It faces punitive tariffs on unrelated exports like steel and electronics, while Western capitals like the US quietly keep buying Russian uranium, LNG, fertilizers, and rare metals, as per the US import data. This isn’t a “gotcha” moment; it’s a data story. Let’s explore if the US and EU’s stance on India-Russia trade is principled or a double standard, highlighting the US-Russia Trade, EU-Russia trade, and India-Russia trade.

Double Standards in the US & EU's Approach to India's Trade with Russia?

The disparity between the US and EU's disapproval of India's expanding trade with Russia, especially in oil, and their continued trading with Russia gives the impression that a double standard is being used. Trade hasn't entirely stopped despite the sanctions and limitations the US and EU have placed on Russia, particularly in vital industries like chemicals, oil, and energy. The claim that they are judging India's conduct differently from their own is strengthened by this selective approach.

Here's a more detailed breakdown:

India's Point of View: India claims that the US and EU purchase more Russian energy and other products than it does, but they nevertheless condemn India for having the same purchasing habits. India claims that it is not making a political statement by increasing its oil imports from Russia; rather, it is doing so to meet its domestic energy needs. A complex supply chain is highlighted by certain Indian analysts, who also note that a sizable amount of the Russian oil that India receives is converted into refined products, a portion of which is then shipped to Europe, as per the customs data on Russia oil exports to India.

Viewpoint of the US and EU: Although the US and EU have placed sanctions on Russia, they have not entirely cut off commercial relations, especially in sectors like energy, where Russia is a significant provider. They contend that their sanctions, which are intended to restrict Russia's capacity to fund the conflict in Ukraine rather than destroy its economy, are directed at particular industries and people. Additionally, they contend that in order to maintain energy security and prevent economic disruption, their trade with Russia is essential.

Important Elements of the Difference

Energy Dependency: India's rising oil imports from Russia are motivated by availability and cost, while the EU's dependence on Russian energy makes a full embargo challenging.

Targeted Sanctions: India's commerce is perceived as supporting the Russian economy, while the US and EU assert that their sanctions are strategic and targeted.

Perception of Double Standards: The US and EU are both maintaining trading ties with Russia while denouncing India for comparable behavior, which gives rise to the idea that there are two different sets of rules.

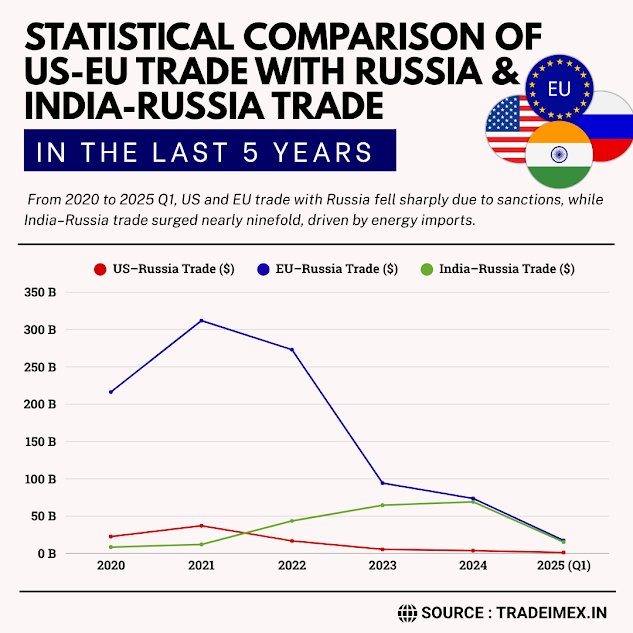

Statistical Comparison of US-EU trade with Russia & India-Russia Trade in the Last 5 Years

|

Year of Trade |

US-Russia Trade ($) |

EU-Russia Trade ($) |

India-Russia Trade ($) |

|

2020 |

$22.65 billion |

$216.33 billion |

$8.48 billion |

|

2021 |

$37.08 billion |

$312.03 billion |

$12.02 billion |

|

2022 |

$16.78 billion |

$273.03 billion |

$43.54 billion |

|

2023 |

$5.49 billion |

$94.29 billion |

$64.64 billion |

|

2024 |

$3.79 billion |

$73.71 billion |

$69.14 billion |

|

2025 quarter 1 |

$1.25 billion |

$17.42 billion |

$15.30 billion |

Despite sanctions rhetoric, the EU and U.S. have maintained billions in trade with Russia, often exceeding India’s levels, revealing a clear gap between public principles and economic practice.

From Outrage to Exceptions: The Sanctions Timeline

In the immediate aftermath of the Ukraine invasion, Western leaders announced sweeping measures to sever economic links with Russia:

-

US sanctions targeted Russian banks, oligarchs, and exports of oil, coal, and technology.

-

EU sanctions included bans on coal, most oil imports, luxury goods, and high-tech exports.

-

Both pledged to phase out dependence on Russian energy entirely.

The rhetoric was uncompromising. But when the sanctions lists were drawn up, certain products, often the ones hardest to replace, were quietly spared.

Why did this happen?

Because full decoupling from Russia was never realistic without triggering domestic crises:

-

For the US, Russian uranium fuels 20% of its nuclear power capacity.

-

For the EU, Russian gas heated millions of homes and powered industries.

-

For both: Fertilizers from Russia and Belarus are critical to agricultural supply chains.

The Numbers: What the US & EU Still Buy from Russia

Let’s look at actual trade data from 2024–2025.

United States

|

Commodity |

2024 Import Value |

2025 (Jan–May) Trend |

Notes |

|

Fertilizers |

$1.1B |

Up 21% YoY |

Higher than pre-war levels |

|

Palladium |

$878M |

Slightly down |

Critical for catalytic converters |

|

Enriched Uranium |

$624M |

Minimal drop vs 2021 |

Waivers until 2028 |

|

Aircraft Engine Parts |

$75M |

Ongoing |

Despite defense sanctions |

In 2024, these four categories accounted for 90% of all U.S. imports from Russia, a total of just over $3B, down from $30B in 2021 but still strategically vital.

European Union

|

Commodity |

2024 Import Value |

Share of EU Imports |

Trends |

|

Fertilizers |

$1.81B |

30% |

Up from 17% in 2022 |

|

Pipeline Gas |

1.6 bcm |

11.6% |

Down from 150 bcm in 2021 |

|

LNG |

€3.5B |

16% of LNG imports |

Up ~12% in 2024 |

|

Enriched Uranium |

2,800 tons |

— |

Significant dependence |

Even after cutting imports by 86% since 2021, the EU still traded €67.5B with Russia in 2024, far more than the US.

The Loopholes: How Sanctions Are Bent Without Breaking

The persistence of this trade isn’t due to blatant violations but rather carefully engineered exemptions and routing tricks.

Waivers and Grace Periods

-

The US uranium ban (2024) comes with exemptions until 2028, citing energy security.

-

EU LNG imports faced no hard ban until March 2025; even then, only transshipment was restricted.

Shadow Fleets

Oil moves via untraceable tankers registered to shell companies in the UAE, Turkey, or Hong Kong, masking Russian origin.

Third-Country Routing

Dual-use electronics, chemical intermediates, and even luxury goods move through Kazakhstan, Armenia, and Turkey before arriving in Russia or from Russia to Western markets.

“Humanitarian” and “Food Security” Exceptions

Fertilizers and certain agricultural products are exempt from sanctions under the argument that restricting them would cause famine in the Global South.

The Hypocrisy Argument: India in the Crosshairs

While the US and EU maintain these trade lifelines with Russia, India has been singled out for criticism.

India’s Position

-

In 2024, India imported $36 billion worth of Russian oil (13% of Russia’s fossil exports).

-

India refines this oil and exports products, sometimes to Europe itself.

-

India faced US tariffs of up to 50% on unrelated goods like steel & electronics.

Western Narrative

India is “undermining sanctions” and “prolonging the war” by buying Russian crude.

The Reality

-

The EU, in 2024, still spent more on Russian LNG and fertilizers than India did on oil.

-

US dependence on Russian uranium is proportionally greater than India’s oil dependence.

-

India points to this as proof of selective enforcement, rules that the West bends for itself but uses rigidly against others.

Country-by-Country Reality Check

United States

-

Imports: Uranium, palladium, fertilizers. (as per the data on Russia exports to US)

-

Rhetoric: “Energy independence,” “support for Ukraine.”

-

Reality: Core imports are exempt until replacements are found—possibly years away.

Germany

-

Imports: LNG, fertilizers.

-

Rhetoric: “Cutting dependence on Russian gas.”

-

Reality: LNG volumes from Russia rose in 2024 before bans took effect.

France

-

Imports: Uranium via Orano, LNG.

-

Rhetoric: “Leading green transition.”

-

Reality: Still buying Russian nuclear fuel for reactors.

Belgium

-

Imports: LNG (transshipment hub).

-

Rhetoric: “Neutral facilitator.”

-

Reality: Moved Russian LNG to third markets until March 2025.

Hungary

-

Imports: Pipeline gas under exemptions.

-

Rhetoric: Openly opposed to strict EU sanctions.

-

Reality: One of the few countries with an explicit pro-Moscow energy policy.

Why Fertilizers & Uranium Are Untouchable

These commodities highlight the limits of sanctions.

Fertilizers

-

Russia & Belarus: among the top global producers of potash, ammonia, and urea.

-

Cutting supply would spike food prices globally, especially in Africa and South Asia.

-

UN quietly urged sanction exemptions to avoid famine.

Uranium

-

Russia controls 20% of global enrichment.

-

Several US and EU reactors are designed for Russian fuel.

-

Building alternative capacity will take 5–10 years.

The result? Long grace periods and waivers, policies publicly framed as temporary, but economically entrenched.

Global Food & Energy Security Risks

Food

-

Fertilizer prices surged 80–120% in 2022 after the war began.

-

Many countries faced reduced crop yields.

-

Even partial disruption of Russian exports could cause another price spike, politically risky in the West.

Energy

-

A full ban on Russian LNG could raise European prices by 30–40%.

-

Gas storage buffers in the EU are temporary; next winter, without Russian gas, will test energy resilience.

Principles vs. Pragmatism: The Political Messaging Gap

Public Messaging:

-

The US & EU: We’re united against Russia. We’ve cut most ties. The pain is worth it for democracy.

Quiet Reality:

-

Certain imports are too strategically important to give up immediately.

-

The phase-outs are slow, and exemptions are large.

-

Trade still flows, just in quieter, less visible forms.

The Hypocrisy Problem:

-

Criticizing India (or China, Turkey, etc.) while keeping one’s strategic imports creates a credibility gap.

-

It fuels perceptions in the Global South that sanctions are not about universal principles but about protecting Western economic interests.

What Comes Next?

The EU’s REPowerEU plan and the US’s domestic uranium enrichment push aim to close these dependencies by 2027–2028. But until then, expect:

-

Continued Russian fertilizer exports to the West.

-

Ongoing uranium shipments to the US and parts of Europe.

-

LNG and pipeline gas are flowing to certain EU states under exemptions.

-

Criticism of other nations for doing what the West is still doing, just in different commodity categories.

What the U.S. & EU Continue Importing from Russia After the War & Sanctions: What’s Not Widely Discussed

Despite the Russia–Ukraine war and multiple sanctions packages, both the United States and the European Union maintain certain imports from Russia, as per the Russia customs export data. Many of these persist due to strategic needs, contractual obligations, or loopholes that make enforcement difficult.

United States

Key Imports (2024–2025)

-

Enriched Uranium: Still a critical input for the nuclear energy sector. By mid-2025, imports exceeded $596 million, with only a small decline compared to pre-war levels.

-

Palladium: Used in catalytic converters and electronics. Imports in 2024 were around $878 million, down from 2021 but still substantial.

-

Fertilizers: Valued at about $1.1 billion in 2024, with a sharp increase in early 2025.

-

Aircraft Engine Parts: Around $75 million in 2024.

-

Other Items: Metals, chemicals, specialty electronics, precision instruments, and niche goods such as vacuum tubes and audio equipment, as per the US-Russia bilateral trade.

Reality vs. Policy

-

The U.S. passed a law banning low-enriched uranium imports from Russia in 2024, but waivers allow continued purchases until 2028.

-

Strategic commodities like palladium and fertilizers are excluded from immediate bans, reflecting selective enforcement.

European Union

Overall Decline, But Continued Trade

-

EU imports from Russia have fallen by about 86% since early 2022, but some sectors remain active.

Key Ongoing Imports

-

Fertilizers: Russia remains the EU’s top supplier, providing roughly 30% of imports in 2024 (up from 17% in 2022). The annual value was around $1.8 billion.

-

Natural Gas & LNG: Pipeline gas imports dropped from over 150 bcm in 2021 to about 52 bcm in 2024. LNG imports from Russia grew by 11–12% in 2024, making up roughly 16% of the EU’s LNG supply.

-

Enriched Uranium: 2,800 tonnes imported in 2024, supporting nuclear plants in countries such as France and Hungary.

-

Oil: Some crude imports continue under exemptions, especially in Hungary and Slovakia.

Policy vs. Practice

-

Plans exist to phase out Russian fossil fuels by 2027–2028 and end existing contracts by early 2028.

-

Until March 2025, LNG shipments still moved through EU ports to other destinations, bypassing sanctions.

Sanctions Evasion and Trade Routes

-

Shadow Fleets: Tankers registered under third countries, often in the Middle East, move Russian oil covertly.

-

Third-Country Re-exports: Turkey, China, and Kazakhstan serve as intermediaries for goods that may be of Russian origin.

-

Dual-Use Technology: Certain electronics and industrial components still reach Russia via indirect corporate structures.

-

Specialty Legal Exports: High-end Russian goods, like studio microphones, continue under allowable trade categories.

Double Standards and Geopolitical Contradictions

-

The U.S. and EU have criticized other nations, particularly India, for buying Russian commodities. Yet in 2024, the EU’s trade with Russia still totaled about €67.5 billion, and the U.S. preserved key imports like uranium and fertilizers.

-

India, which imported about $36 billion in Russian oil in 2024, faces higher U.S. tariffs on unrelated goods, while Western nations quietly maintain their trade flows.

-

Many sanctions focus on sectors with symbolic or military importance but spare critical commodities tied to domestic economic stability.

Implications for Global Markets

Fertilizers

-

Russia and Belarus are among the world’s largest fertilizer exporters. Restricting trade risks food inflation, especially in developing countries.

-

Global organizations have pressured the West to keep the fertilizer trade open to avoid agricultural crises.

Energy

-

Russia remains a top LNG supplier globally. A sudden cutoff would raise prices sharply, so reductions are gradual.

-

Europe is investing in energy diversification, but full independence from Russian supply is years away.

Nuclear Sector

-

Rosatom controls a major share of global uranium enrichment and reactor construction.

-

Many reactors in Europe, including new builds, are Russian-designed, making a short-term supply cutoff unrealistic.

Summary

|

Region |

Key Imports (2024–2025) |

Trends |

Policy Actions |

Double Standard? |

|

U.S. |

Uranium ($624M), Palladium ($878M), Fertilizers ($1.1B) |

Fertilizer imports rising; uranium drop minimal |

Uranium ban with waivers until 2028 |

Publicly tough, quietly dependent |

|

EU |

Fertilizers ($1.8B), Gas/LNG (19% share), Uranium |

Fertilizer share up to 30%; LNG imports increased in 2024 |

Tariffs, phase-out plans by 2027–28 |

Criticizes others while delaying full cutoff |

The Takeaway

This isn’t to say sanctions have been meaningless; they’ve cut Russian-European trade by over 80% and reduced Moscow’s fossil fuel revenue from Europe. But the narrative of total economic isolation is misleading.

The facts:

-

The US still imports hundreds of millions in Russian uranium, palladium, and fertilizers.

-

The EU still buys billions in fertilizers, LNG, and uranium.

-

India, while criticized, imports less in relative terms than these Western blocs.

If sanctions are about principle, then principles should be applied evenly. Otherwise, they become another instrument of selective power, rules for some, loopholes for others.

Conclusion and Final Verdict

In conclusion, the trade relationships between the US and EU with Russia and India are influenced by a complex interplay of factors, including geopolitics, human rights concerns, and economic considerations. The circumstance demonstrates the intricate interaction of political, strategic, and economic factors. Both the US and the EU have solid justifications for their actions, driven by their own national interests and energy demands, despite India's accusations of unfair treatment. Meanwhile, India’s point is also a strong one regarding the US and EU’s double standards on trade with Russia. Despite the criticism, the continued trading relationship with Russia shows that even for great powers, total trade isolation is challenging to attain.

We hope that you liked our insightful and data-driven blog report. For businesses, policymakers, and analysts seeking to navigate this opaque trade environment, TradeImeX offers access to search live import–export data of 100+ countries. To explore accurate, up-to-date trade intelligence, contact us at info@tradeimex.in and get a customized database report as per your business needs.

Share

What's Your Reaction?

Like

2

Like

2

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0